What is Stack?

Own Your Health.

The US healthcare system is the most urgent and pressing problem impacting the US economy. US consumers, taxpayers, and employers spend roughly $5T every single year on healthcare, which is over 18% of our GDP. Beyond the absolute cost, the growth rate is unsustainable, as health spending is growing faster than the economy is growing. Health insurance premiums are growing almost 3 times faster than wage growth. As healthcare dominates an ever larger share of our nation’s balance sheet, it will accelerate deficit growth, raise our borrowing costs, and risk trapping the US in a negative feedback loop of taking on catastrophic levels of debt in order to fulfill our healthcare obligations.

So, I’ve started a new company called Stack Health to solve this problem with the urgency it requires.

Americans are struggling to pay for the costs of healthcare. The premium for a family of four in the US is now $27,000 a year, and rising fast. Employers, especially small businesses, are straining under these costs as they cover much of the premiums to attract and retain talent. Worse yet, rural hospitals are failing at an alarming rate, 37% of hospitals are losing money, and admin costs now consume $1T in annual spend. This is truly an existential moment for the affordability of American healthcare, and it starts with challenging the fundamental unit of risk for about half of all Americans: the employer.

The US needs to evolve employer health coverage to a tailored, individualized market, empowering each person to own their health.

What will this look like? Stack represents a new era of individual sovereignty in healthcare with an approach that migrates members to their own policy, customized to risk and needs, creating control and accountability while sharing values and mission collectively. When individuals own their coverage, the market can price risk accurately and reward healthy behavior. Stack’s approach will help lower prices, eliminate middlemen, and radically increase freedom and transparency in the system.

By removing the employer and its various intermediaries from the equation, it will bring the dollars (and choices) down to the individual level, resetting the entire system onto a new foundation just in time for a dramatically different, dynamic, and decentralized health industry to take hold. Functionally, individuals can shop and negotiate for themselves in a way their employer can’t, and match their healthcare spending decisions to their risk tolerance, anticipated health needs, and personal budget. This transformation, combined with administrative automation amongst payers and delivery infrastructure, should be able to lower costs by 25%+ over time without compromising quality; in fact, in many cases the market will be able to improve outcomes, experience, and cost efficiency at the same time.

The second order effects are just as exciting: more small businesses can start and scale due to more affordable worker costs, and employees will finally have true portability to be able to confidently change jobs freely, or freelance/contract when desired. As a founder myself, I believe deeply that startups and small businesses are the best way to grow employment and opportunity for people, and I want this sector to thrive.

Over the past 13 years, I served as the CEO and co-founder of my first company, Beam Benefits, which has become a leader in the small business employee benefits industry. Despite our success and scale at Beam, I’m compelled to help our country and fellow citizens in a new way, leveraging my experience and network on a deeply important and meaningful new mission.

At Beam, we created a first-of-its-kind pricing model that offers better prices to small businesses and gives them credit for having lower risk characteristics. We also noticed that dentistry operates much closer to a retail model, where dentists compete to lower prices, where those prices are more transparent, and patients are free to go to the dentist of their choice. Everything I have learned building Beam is present in Stack, from insurance infrastructure, prudent risk management, small business distribution techniques, and excellent user experiences.

I believe that market forces like HSAs, price transparency laws, direct primary care, portability, defined-contribution benefits, and most of all, artificial intelligence, make this a uniquely timed, generational opportunity to build one of the most consequential companies of this decade and beyond.

What is Stack?

Stack Health is the operating system for personalized health plans to accelerate the transition to coverage being owned by individuals instead of employers. Stack helps our members visualize their healthcare as a ‘stack’ of products that all come together in a seamless way to create a customized and comprehensive approach to healthcare.

Today, around 160 million Americans are getting something much more generic in the form of an employer-sponsored health insurance policy. Separately, tens of millions of Americans are purchasing and engaging with consumer health products, ranging from wearables to supplements to fitness platforms to mental health tools to primary care subscriptions to discount drug cards to sleeping aids, and much more, which aren’t typically covered by health insurance. Simultaneously, many large employers are struggling to get engagement with digital health point solutions that are only a fit a small percentage of employees and difficult for HR infrastructure to adequately support.

All these problems and more are addressed by Stack Health’s solution, which builds the benefits program for each individual, to fit each person’s healthcare needs, budget, and risk tolerance. Instead of trying to find a health insurance product that covers each and every potential interaction with the healthcare ecosystem, Stack determines the most likely and most impactful care modalities for the coming year and designs the individual’s Stack accordingly.

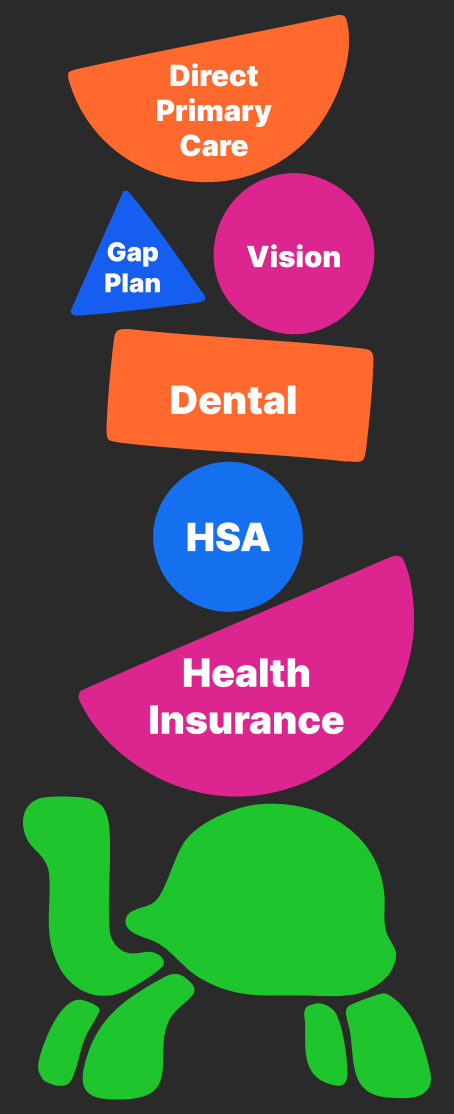

The solution set contains an ever-evolving marketplace of the latest and greatest point solutions across digital health, tax advantaged financial products like HSAs, compelling primary care partnerships, and multiple ways to integrate dental and vision coverage into the program. At the base for all members is their ‘shell,’ an individual health insurance plan focused on protection against large, unforeseen health events (like a car accident or cancer diagnosis) that can create bankruptcy-level financial risk.

In aggregate, this approach is not only more personalized but also much more efficient than an individual trying to build their own healthcare stack or by relying on employers to be able to thoughtfully construct something of equal quality for each person.

Any given member’s Stack may include:

An insurance plan from the ACA market

‘Gap’ products to cover the member’s deductible

Health Savings Accounts (HSAs)

Direct Primary Care access

Dental and Vision coverage

Digital health point solutions

We expect that our members will interface with Stack through a mix of traditional user interfaces, agentic tools, and humans in the loop. In aggregate, these tools guide them through a highly differentiated care experience. Demonstrating this are 3 key ‘moments that matter’ in the customer journey:

Stack manages the enrollment process for all products through a single, unified user experience, allowing members to achieve all coverage tasks through a single interface.

Stack’s care navigation tools guide the member to select the right service, doctor, quality level, and timing for care based on the context and criteria for that specific care episode. There are often multiple and ambiguous ways to accomplish a given task that may have different financial outcomes, quality or convenience tradeoffs, or other considerations. Modern AI capabilities can now provide contextual and conversational support in these instances that would not have been possible even 30 months ago.

In the clinical environment, Stack uses an intelligent health wallet to assist in organizing prior authorization, billing, and payment in the most efficient and effective way possible, giving members decision and negotiation support along the way.

Stack’s incentives are aligned with our members to find the lowest possible cost of care. Stack only makes money when employers like our services (paying us a small subscription fee to set up Stack for their team), and when our members engage with useful products and tools that help them find the lowest cost of care.

Who is Stack for?

Stack will initially target the small and medium-sized business (SMB) market. About 90% of SMBs with under 10 employees don’t offer health insurance today. In fact, only 53% of firms with 10–49 employees offer health insurance as well. Why? Most micro-employers under 50 lives don’t meet fully insured enrollment requirements, and they don’t legally have to offer health insurance due to their size. This is an ideal use case for why Stack can matter so much to the employees of these businesses. Today, these employees are mostly left to fend for themselves, choosing between ACA marketplace plans with little to no support, jumping on their spouse’s plan often at great expense, or going without insurance at all.

For SMBs that do offer health coverage today, costs for traditional, fully-insured group plans are $500-900 per person per month in most markets, and prices are increasing ~10% annually, well above inflation and GDP growth. In as many as 33 states today, the fully-insured plans are more expensive than similar quality ACA Marketplace alternatives. I believe this will be more true, in more places, over time.

These employers can now offer a defined contribution plan (called an ICHRA) to set an allowance. Though it’s a small market today (~500K participants growing 50% YoY), this will accelerate due to subsidy expirations, fully insured cost increases, and other pressures forcing businesses to rethink how they budget and manage risk. With these defined contribution plans, employers set their allowance per employee, so it provides predictability, and often substantial savings.

For example, an employer may be currently spending an average of $750 per person to provide a traditional group health insurance policy. With a defined contribution plan through Stack, the employer may now choose to set an allowance of $600 per person, producing savings and a capped allocation upfront, while still making a significant investment such that the employees feel the employer is meeting their expectations for providing healthcare coverage.

As more employers choose to unplug from the healthcare matrix, the net effect is both good for the employer, their employees, and the system itself. In reality, the average healthiness of individuals in the employer market today is quite high, but employers are typically building a solution for the whole company, which often means a majority of the workforce is overinsured. These members are sending money to insurance carriers that could be spent more efficiently on other health services or products, instead of just insurance coverage. These people will now purchase products individually that lead to much more choice and competition for a wide variety of products and services across the healthcare spectrum. The risk pool of individuals gets bigger, and healthier, as workforce- age individuals join the individual marketplace as a first option instead of a last resort. In general, this lowers prices of the risk, decreases distribution costs, and increases the number of options. This induces more employer conviction and the individual health coverage market flywheel turns faster.

Stack will also partner with freelancers, or self-employed independent professionals (like creators, entrepreneurs, consultants, etc). This is a sizable audience, around 8 million Americans today, 5 million of whom just don’t buy insurance at all, and 3 million who purchase individual plans today. For this group, comprehensive coverage is really expensive, and support in the purchasing and navigation of care is minimal. Stack introduces a product tailored for this audience in select markets to help this group with a level of support and infrastructure that is extremely rare to find in today’s market.

Why Stack Matters

Why is our healthcare industry so broken? Being dismayed by our system is a rare topic that nearly everyone seems to agree on, and everyone is looking for someone to blame. But, it’s not about the people, or the component parts; it’s the incentives that fuel the system itself. All of healthcare’s myriad stakeholders are just following their incentives and to varying degrees, want to keep things the way they are. But, we now may be on the cusp of major change.

Three catalysts emerged for the first time in 2025 that I believe mean a significant acceleration of improvements to healthcare is now possible.

The first is technological change; the generative intelligence moment we are living in opens up significant new pathways for organizing data, automating back-office workflows, and providing context and support for decisions that were previously either not possible, or extremely difficult to scale at the consumer level.

The second catalyst is cultural; ‘healthcare is broken’ has been a refrain for decades, but only recently have prices for employer-sponsored plans become truly punitive and represent a 25%+ drag on new business formation and job mobility. After all, today’s health industry contains many perverse incentives, due in part to the scale of employer-sponsored insurance, which means insurers in general do not want to pay for longer-term treatment and prevention for members who will switch employers, and therefore switch to another carrier. Consumers have started to rebel, leading to counterculture movements including Longevity science (peptides, supplements, diets, etc), Make American Healthy Again in the political context (giving voice to skeptics of the underlying science and institutional rot around public and population health initiatives), and at least one high profile act of violence motivated by the frustration with today’s system. Increasingly, consumers are taking matters into their own hands, finding ways to get on GLP1’s, leveraging LLMs for health related questions and needs, and seeking treatments outside the traditional medical system.

The third is regulatory and policy catalysts, which include Price Transparency laws, expansion of direct primary-care and HSA access, the creation and expansion of defined contribution plans for employers, and much more. The foundational components for a consumer-first healthcare era are mostly in place at this point, more than enough to create system level change in a compressed time frame.

***

Companies like Stack Health must be built now. Whenever I drive by a new wing being added to an already huge hospital, I’m reminded of the centralization that’s been the driving force of modern healthcare. There’s one major EHR system, 5 large carriers (all with their own PBM and care delivery infrastructure), and increasingly a few large health systems that dominate metropolitan areas all over the country.

It’s time for a punk rock revolution to the system; a reaction that is brash, aggressive, and truth-seeking. Today’s system has become sluggish, bureaucratic, and consolidated. Punk was a democratizing force against the corporate music elite, and proved that simplicity and honesty were key ingredients in making music that connected at a raw and emotional level with people. The gritty and rugged feel of the artists felt close to the people consuming the music, not a far-away stage in a massive arena.

I believe that nothing will truly change about our healthcare system until the patient is the predominantly responsible party for their own healthcare. As long as the average person is on the receiving end of someone else’s decisions and wallet, there will continue to be a fundamental mismatch between the consumer and all other stakeholders.

Stack Health’s vision is to empower every American to own their health and create a more productive and prosperous society. We will do this by creating value, staying with our members over the long-term and helping through the whole lifecycle of care with a range of consumer tools, not just shopping for and selecting an insurance plan. Stack brings a concierge medicine experience to all consumers and performs roles that are distributed across the healthcare industry today in a unified way, with all the context and ability to synchronize the right medical decision with the right financial one. I believe that Stack is good for the healthcare consumer, for American small businesses, entrepreneurs, freelancers, and the health of our economy.

In this newsletter, I’ll be sharing more about the genesis of the original idea for Stack, detail our product features in more depth, introduce more context about the historical urgency of this moment in our healthcare system, and make the case for elegant and bipartisan updates to healthcare policy that can clear the pathway for a more functional, efficient, and lower cost health industry.

If you align with Stack’s vision for all people to own their health and you would like to explore our products for yourself, your company or your book of business, you can also join our wait list here.